New act on SA: a “headache” or a «business opportunity»?)

Ι. Preamble

Felix Hoffmann (1868–1946) was a famous German chemist.

His name went down in history as the creator of, among others, a preparation intended to cope with headaches (the “aspirin”).

The commercial success of the aspirin was, as we all know, huge. It was destined to be legendary -up to today. (As a result of its success, the aspirin is exhibited in the national Museum of American History of the Smithsonian Institute, in Washington.)

The fact that the aspirin successfully cures headaches is, to this day, a given. The only headache it cannot cure is that which comes with businesses. And it is a big one…

The new act on S.A.s has been in force, as it is well known, since 1.1.2019.

But is it just one more “headache” or a (once in a lifetime) business opportunity?

An act of a hundred and ninety (190) articles, a sixty-eight (68) page long act (pages in the Government Gazette) could not be analysed in just one article. This is not what we intend to do. But it is quite important to focus on the business aspect of it all. We will attempt to tackle the most important and most common practical issues that arise when dealing with an SA.

The approach taken in this article will help realize how an act can turn into a business opportunity….

(or not?)

ΙΙ. A little backstory

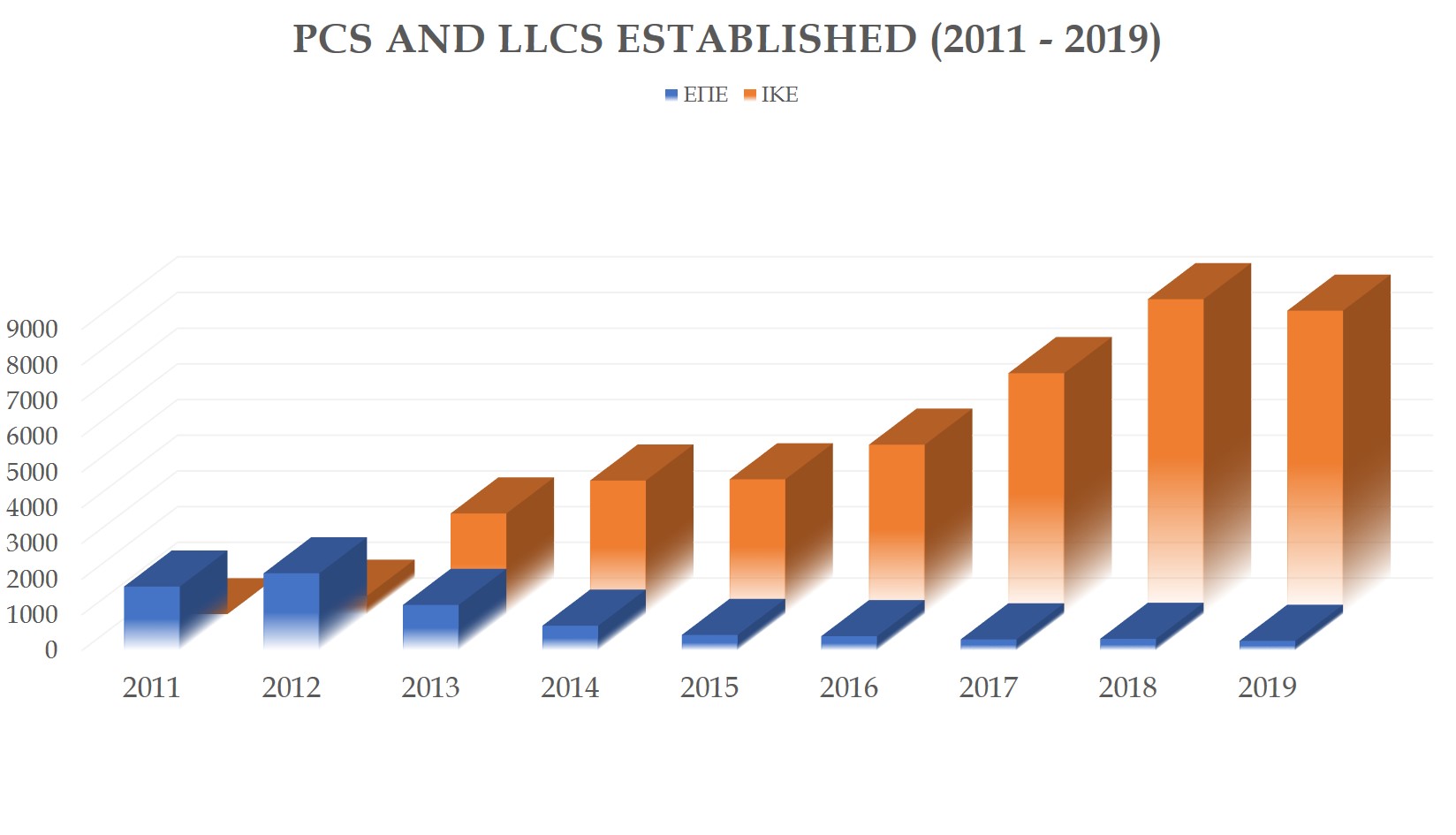

New act on SA – no. 4548/2018 (which replaced act 2190/1920) is very modern and up-to-date.

But what was act 2190/1920? The second half of its name confirms that it was passed in 1920.

Early 20th century, this act was indeed ground-breaking in the field of company law. But with decades passing after it came into force, amendments were necessary in order for it to remain relevant. Some of them, major. And with the decades passing, the withdrawals, amendments, interventions and additions started piling on. Because going back to the provisions in place and “tweaking” them was not enough, we started adding new ones (e.g. articles 42, 42Α, 42Β, 42C, 42D, 42Ε). Those “adjustments” ended up being so many, that so few elements reminding of the initial act were left. Some provisions seemed to just be “thrown in there”, with no cohesion with the rest of the act. The act ended up being a true patchwork…

Its replacement was a necessity.

The hundred-year-old 2190/1920 already gave its place to the “young” 4548/2018. With the latter already in force for ten months now, we are in a place to come to some useful conclusions.

ΙΙΙ. “Ignorance of the law” and “one size fits all” articles of association

Since ignorance of the law is not forgiven, no one can claim they are above the law.

What was happening until 31.12.2018? And what is happening now?

Businessmen, with only a few exemptions, were completely ignorant when it came to their own company’s articles of association. Unfortunately, so did most of their advisors. Most articles of association were not “made” to serve the specific needs of each businessman. Minor amendments to the (statute) model-texts notaries had once drafted proved(?) enough. And the (new) SA was ready to go!

But when a problem “knocked” on the SA’s door, the businessman would “knock” on a lawyer’s door. And the latter would turn, for the first time, to the articles of association.

In most cases, that was TOO LATE…

That is when the businessman would realize that they should carefully and properly amend their articles of association (and often this realization would come with a painful and unnecessary cost).

IV. Business view of Societes Anonymes

We have already seen in the introduction that such a long act (as is act 4548/2018) could not be analyzed (or even presented) in one article. But we sure can attempt to approach the most common and practical aspects of the act, at least from the business point of view. A decalogue would come in handy for businessmen and their advisors.

Let’s take it one step at a time:

-

A fast and, foremost, cheap start

An SA can now be established in minimum time and with an close-to-zero expense.

Since 2016 (article 9 act 4441/2016) the participation of a notary and a lawyer often proved redundant.

The SA can now, in some cases, even be established with a private document (article 4 § 2 act 4548/2018). A necessary requirement is to be using the official model articles of association and submit it to the relevant “one stop shop” of the Business Registry. An important prerequisite: to not diverge from the official model. Small (?) detail: the “one stop shops” still only have available models drafted according to the (abolished since 1.1.2019) act 2190/1920…

In more complex cases (as well as in cases where the founders wish to divert from the provisions of the official model) the SA can only be established with a notarized document. A notarized document is also required when a legal provision specifically calls for it, or if contributions in kind are made to the company, contributions that in order to be transferred a notarized document is required (article 4 §2 act 4548/20190).

But still in cases where the articles of association can only be valid if they come in a notarized document, there is a way to minimize costs. Choosing small (size-wise) articles of association – by avoiding unnecessary repetitions of the law, is the best practice. The cost (at least of the official copies) will be significantly smaller. And even more so: possible amendments of the law will not create a need to amend the articles of association accordingly.

-

Attracting and keeping capable executives

It is extremely important for all businesses to achieve, among others, a triple goal:

- Attract capable executives,

- Keep them for a long time,

- Minimize their cost.

Businesses and their executives have, in most cases, contradicting interests -and both sides want to mainly serve their own.

Executives want to receive, in most cases, bigger salaries and other benefits.

Businesses want to give out lower salaries and minimize other relevant expenses. They also have medium- and long-term targets.

When the conflict of interests between management and ownership minimizes, at least by a little, everything becomes simpler. But what is the way to do so in an SA?

New Act on SA – 4548/2018 offers multiple opportunities to SAs, in order for them to successfully tackle the (given) conflict of interests between them and their executives. Some of them are the Stock Options (article 113 act 4548/2018), Bonus Shares (article 114 act 4548/2018) and/or Ordinary Founders’ Shares (article 75 act 4548/2018).

In cases of Stock Options and Bonus Shares, the executive is offered a chance to become a shareholder (with or without monetary consideration). This new role (that of a shareholder) is offered either at the time the executives are hired or after they have already established a long-term relationship with the SA. This way the interests of the SA and an executive align.

It is a bit different with Ordinary Founders’ Shares. Those shares are offered, among others, to executives at the time the SA is established. The owner of an Ordinary Founders’ Share will be hoping for the improvement of the company’s economic outturn. This (improved) economic outturn is what it will bring for them the agreed upon profit. But the shareholders do not carry any risks regarding the shareholding balances: Ordinary Founders’ Shares do not carry rights equal to those typical company shares do (e.g. voting rights or participation in the management). At the same time, the dividend their owners can receive is maximum ¼ of the amount exceeding the minimum distributable dividend. In any case, Ordinary Founders’ Shares do manage to align the interests of executives and the business.

-

Minimizing company expenses and shareholder disbursements

Any business’s goal is, among others, the improvement of its cost-benefit ratio. This goal can (also) be achieved by minimizing costs. The shareholders aim to improve the company’s economic result. At the same time, to have to withdraw as less money as possible. The interests of a company and its shareholders are often perfectly aligned, sometimes identical.

The recent act on Société Anonyme offers tools to achieve the abovementioned goals.

We have already referred (above under 1) to the deduction of cost at the stage of a company’s establishment. Adopting the formal model articles of association and not involving a notary or a lawyer is a step to that direction. But what happens if a notarized document is required? Short articles of association with no repetitions of the law.

But how can one minimize expenses when a company operates?

We have already mentioned the tools the law provides for the minimization of salary expenses (above under 2).

A relevant tool (for minimizing expenses) is the utilization of technology. The recent act offers significant opportunities for the utilization of technological tools. Opportunities not at all insignificant, that will not only boost effectiveness, but also minimize operating costs.

And as far as shareholders are concerned, is it possible that they will have to suffer fewer financial burdens and make less withdrawals?

The partial payment of the SA’s capital (article 21 § 1 act 4548/2018) is the tool to do exactly that. The partial payment of the capital can take place, under certain conditions, not only at the stage of an SA’s establishment, but also in cases of capital increases. By taking advantage of this opportunity, the shareholders can deposit in the company only a fraction of the capital they have taken on to cover. They can postpone the obligation to pay off the rest of it, thus facilitating the management of their finances.

-

Attracting investment capital

The expectations businesses once had, that banks would provide financial support, is well in the past.

Attracting investment capital is now a pressing need.

The act offers significant options and tools that will accommodate such needs.

The tools offered are (among others):

- Warrants (article 56 act 4548/2018), which offer the right to those who hold them to acquire, sometime in the future, shares of the company which issued them, in a pre-determined, low price.

- Preference Shares (article 38 act 4548/2018) can offer a wide range of privileges. Receiving dividends before ordinary shares, receiving interest and having a priority when it comes to participating in a company’s profits that derive from a specific business activity are only some of them. Preference Shares can either incorporate or not voting rights.

- Redeemable Shares (article 39 act 4548/2018) offer the right to their owners to request to have them, sometime in the future, bought by the company which issued them, in a beforehand agreed upon price.

- Bonds (article 59 et seq. act 4548/2018).

- A combination of the above “tools”.

-

Drawing liquidity from the Société Anonyme

Part of the (Greek) reality is the “utilization” of company cash, for covering needs of its shareholders. But a Company’s Cash and the Businessman’s “Pocket” are two different things. A possible blurring of the boundaries between the two will create multiple and extremely severe risks. For the business, as well as for the businessman. This is why “informally” obtaining liquidity from a company should be avoided. There are several tools, though, to help make it “formal”. A necessary prerequisite is the support of the majority of the shareholders and the ability of the company to respond.

The most common tools are: (a) for the members of the Board to participate in the company’s profits, and (b) the conclusion of contracts between the SA and its major shareholders, BoD members and related parties (even more so since the previous provisions of the act have been abolished).

As significant (if sometimes not more significant) as the above tools are, among others, the following:

- The distribution of dividend (final or interim),

- The Deduction of the Capital (articles 29 et seq. act 4548/2018),

- The Amortization of Capital (article 32 act 4548/2018),

- The issuance of Ordinary Founders’ Shares (article 75 act 4548/2018) and

- The issuance of Extraordinary Founders’ Shares (article 76 act 4548/2018).

-

“Managing” small shareholders

New Act on SA – 4548/2018 strengthens, as it seems, the rights of the minority, especially through the right given to them for exceptional auditing. Nonetheless, the existence and the implementation of the minority’s rights are not always enough to achieve the necessary balance in the relations between the minority and the company. Often, the exit of the minority shareholders from the company is in the best interest of both them and the company.

The minority shareholders can reach the exit by taking five, among others, ways:

(a) By the option given, under conditions, to the minority shareholders (holding ≤5% of the share capital) to request before a court:

(aa) the redemption of their shares by the SA (Act 4548/2019, article 45) and

(ab) to be bought-out by the majority shareholder (holding ≥ 95% of the share capital) -(Act 4548/2019, article 46)

(b) By the option given, under conditions, to the majority shareholder (≥95%) to buy-out the minority shareholders (Act 4548/2019, article 47)

(c) By the increase (ordinary or extraordinary) of the share capital, as well as

(d) By a (combined) decrease and increase of the capital.

-

Utilizing technology

The Act on SAs facilitates, by providing plenty of relevant provisions, the utilization of technology. The use of technology, without it being obligatory, has proven beneficial on many levels. For example, technology can be used in an SA:

(a) for issuing intangible shares and digitally keeping the Shareholder Book (Act 4548/2019, articles 34, 40 par. 2 & 5),

(b) for the board of directors to conduct its business and take decisions (Act 4548/2019, articles 90 & 94),

(c) for shareholders to exercise their rights through emails (Act 4548/2019, articles 122 & 123),

(d) for General Assembly Meetings and forming of the relevant decisions (remotely and by electronic means – Act 4548/2019, articles 125 to 128, 131,135 and 136),

(e) for shareholder unions (Act 4548/2019, article 144).

-

Succession

The SA is “the ultimate” capital company. In Greece, though, the majority of SAs are family businesses – heavily resembling partnerships, as per the way they are run.

Almost every family business-SA at some point will have to deal with the issue of succession – the transition to the “next generation”. This issue is often “taboo”.

Succession issues cannot be solved with “absolute truths”. But they can be solved if they are approached by mature businessmen and proper advisors.

A great help towards solving succession issues can be drafting “tailor made” articles of association. Those that will:

(a) Set, in advance, reasonable rules for restricting the free transferability of shares. Introduce a procedure that can take place through issuing restricted shares (Act 4548/2019, article 43). The restrictions apply on all transfers, including the ones owing to the death of a shareholder.

(b) Regulate (in the most appropriate way and reasonably) the exercising of the rights of the minority. Also, the rights of minority shareholders concerning auditing.

-

Protecting the investment

Attracting investment capital is not enough.

The shareholders and administrators of an SA have the obligation to protect it.

As already mentioned, carefully worded, “tailor made”, articles of association will play a significant part. Those articles must carefully set the proper boundaries in the relationships between shareholders, in order to avoid internal disputes.

The rights of the minority shareholders and how they are exercised must, in this case as well, be carefully defined. Even more so when it comes to the rights of the minority shareholders concerning auditing.

Another important issue for most SAs is securing the “next day” and the business venture, meaning securing the company’s and the existing shareholders’ interests. A possible transfer, i.e. of company shares to a competitor would, most likely, not be at the interest of the company. A provision for restricted shares appears to be necessary here as well.

Establishing the reasonable (and probably necessary) restrictions that are the Tag Along Right and the Drag Along Right seems, in most cases, necessary.

But necessary in all cases are:

(a) The provisions in the articles of association regarding the protection from possible competitive and unfair actions taken by the BoD members, the executives and the shareholders.

(b) The careful selection of the SA’s representatives.

(γ) The careful definition of boundaries of the responsibilities of each one of its representatives.

-

Protecting the owners, directors and executives

The range of the responsibilities of the members of the board of directors is very wide. Civil, criminal, administrative liabilities before the company, before third parties, etc. These liabilities can be put in two large categories:

(a) The responsibilities of the members of the board of directors, according to the Act on SAs

(b) The other responsibilities of the members of the board of directors

The responsibilities of the members of the board of directors cannot be set to zero. But they can be limited. Solutions towards that direction (among others) are:

(a) The reduction of number of the persons involved (i.e. through the provision of a Single-Membere Administrative Body / Consultant-Manager)

(b) The Insurance Of The Liability Of The Members Of The BoD And Of The Executives Of The S.A.

V. The new act on SA as a “headache”

The new Act on SA is, indeed, one more problem for businesses. And even more so, one more “headache” for businessmen. Businessmen have to (if they haven’t already):

- Manage the (smaller or bigger) confusion created in their business.

- Spend money on informing their

- Spend money (i.e. on new articles of association) in order to align the operation of their company with the requirements of the new Act.

- Get informed themselves (in general) and make sure that their advisors (legal, financial, tax) are also informed in detail and familiar with every aspect of the new Act.

VI. The new act as a business opportunity

On the other hand, the new act on SA is a significant business opportunity. With reference to the (necessary) alignment with its provisions, the businessman has the opportunity to reaproach important data. Among others, to search for the best solutions regarding:

- The drastic (and efficient) reduction of cost when attempting new business endeavours,

- The attraction and maintenance of capable executives, while simultaneously minimizing the cost of their salaries,

- The minimization of operational costs and of the shareholders’ withdrawals,

- The (always) wanted and necessary attraction of investment capital,

- The (best suited) solutions in obtaining liquidity from one’s business,

- The managing of small shareholders, something which, in some cases, proves crucial,

- The (multiple) utilization of technology, aiming to the business functioning more efficiently, as well as to saving money.

- The tackling of issues relating to succession.

- The protection of the business and the investment and, mainly,

- The protection of shareholders, BoD members and executives.

VII. Utilizing the business opportunities

There is no question that the new act on SA is a significant opportunity. An opportunity which, if approached in the right way, will create multiple business opportunities.

But how should it be approached?

It is necessary for the businessman to get informed on all the tools provided by law (it goes without saying, no great detail is needed).

It is also necessary for them to confirm that their advisors and associates are in a place to support this endeavour. But the most important thing of all:

It is imperative that they reaproach their SA’s articles of association and have them “tailor made” to their needs. The purpose and end goal should not be to just adjust it to the provisions of the recent act. The purpose should be to utilize the (very significant) opportunities it offers. Few of them mentioned above.

VIII. In conclusion

The recent (implemented since 1.1.2019) new act on SA has been the operative event for many headaches. Businessmen, accountants, lawyers, tax consultants, business advisors, we did not avoid them. (at least not all of us…)

No aspirin could treat, not even partially, a businessman’s “headaches”. The headaches created by the implementation of a new act included.

If the “father” of aspirin (Felix Hoffmann) was alive, he would come to the same conclusion.

With certainty.

It is well-established that the “business opportunities” this act brought with it are more than significant. And multiple, compared to the “headaches”.

All that is left is for us to utilize them.

As soon as possible.

Stavros Koumentakis

Senior Partner

P.S. A brief version of this article has been published in MAKEDONIA Newspaper (November 3rd, 2019).